Guest opinion: a three-tier business model for the global semiconductor industry

It is an open secret that, for a variety of reasons, the U.S. manufacturing base has sharply deteriorated over the past three decades, and the semiconductor industry is no exception. In fact, the semiconductor industry may have suffered harder than some other American enterprises. The purpose of this paper is to explain the causes of this decline and offer some common-sense economic policies that may lead to the industry’s revival.

In the microelectronics area a semiconductor fabrication plant is a factory where such devices as integrated circuits are manufactured. A business that operates a semiconductor fab for the purpose of fabricating the designs of other companies, such as fabless semiconductor companies, is known as a foundry. If a foundry does not produce its own designs, it is known as a pure-play foundry. As of today, the semiconductor industry follows a multinational corporation (MNC) business model based on globalization.

Following World War II U.S. business leaders pursued globalization, believing that American firms would be able to capture foreign markets, but the opposite happened. Other nations imported technology from American companies, and, with their low real wages, out-competed U.S. firms all over the world. The rest is history.

When the recession struck in 2007, the lingering weakness of the American economy came to the surface. With decreased exports and increased imports and the high cost of maintaining U.S. war fronts abroad, the budget deficit has been increasing. Additionally, counterfeit electronics from abroad have raised national security issues.

Multinational corporations have spread their semiconductor production operations across the globe, and since the 2007 recession, the semiconductor industry has observed flat growth in its revenue and many small businesses have experienced a slowdown. Such stagnation has been analyzed in my article entitled Revival of U.S. Electronics and Semiconductor Industry and Mitigation of Counterfeit Electronics through Macro-Micro Economic Policies.

My proposed business model is designed to help restore a balanced economy without having to rely on overseas investment or foreign debt; establish a free-market economy where supply and demand of goods rise and fall automatically with minimal government intervention; solve the problem of unemployment and hence excessive government spending that leads to budget deficits; help the semiconductor business be at the leading edge of technology through sustainable capital investments; and ensure a competitive business environment which would stimulate the growth of small businesses.

A balanced economy is critical to take the global semiconductor industry to the next level of innovation and financial success because it would increase domestic consumer purchasing power. In addition to a balanced economy we also need a decentralized supply chain, which increases co-operation among businesses, decreases wealth concentration in the economy, and improves efficiency and customer satisfaction.

Macroeconomic reforms towards decentralizing the fabless semiconductor business would boost the growth of several small fabless firms in an economic subsystem. Only with a decentralized supply chain does can an individual player flourish. Hence, the decentralized supply chain leads to smaller organizations and a lower probability for mergers and acquisitions. A decentralized supply chain leads to higher co-operation among entities in an industry.

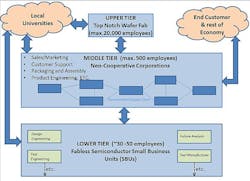

A three-tier model

I propose a three tier model for the robust growth of fabless semiconductors. The entire semiconductor Industry should be split into economic subsystems based on the availability of raw materials. This model is based on what is known as progressive utilization theory or PROUT, which was put forth by Shri Prabhat Ranjan Sarkar in 1959.

The upper tier is a top notch wafer fab and fabless small businesses are a lower tier. The middle and most important tier has neo-cooperative corporations that have exchange relationships in a decentralized supply chain. The middle industrial tier connects the other two industrial tiers with rest of the economy.

A wafer fab needs an investment larger than that of a nuclear reactor. In 2013 the cost of building the next generation wafer fab was estimated at over $10 billion. The location of wafer fab should have ready availability of all necessary raw materials, as well as access to airports and transportation infrastructure for a smooth delivery of the goods to end customers. This would ensure the growth of smaller and medium size businesses, which would cater to that fab. Any infrastructure investment would be a long term investment to attract other businesses.

To have a balanced economy, the official monetary policy should be such that wages keep up with labor productivity. Since workers’ wages contribute to consumer demand and workers’ productivity contributes to the supply of goods, when wages catch up with productivity, supply and demand grow and fall together. To ensure that wages catch up with productivity, there should be special incentives offered to highly productive employees. The remaining profits, if any, should be shared with the private investors as return on their investments. Fabs should have complete autonomy to lay off unproductive employees to stay at the forefront of innovation.

For the semiconductor industry to be financially successful, it is critical that money circulates in the economy. To make this feasible, the fab should offer retirement schemes to enable its employees to invest some of their income towards the growth of their company by purchasing company shares.

This model has two benefits. Since employees own some shares of the fab, they would work hard towards the success of the foundry. In economic downturns, these wafer fabs would prefer to share losses by taking across-the-board wage cuts or by cutting work hours of workers rather than laying them off. A good wafer fab also should collaborate with local universities by offering co-operative internships to engineering students and technicians.

Lower tier

An established wafer fab also would create local businesses, which provide necessary tools, test equipment, and engineering services. These providers would form Lower Tier of this three-tier business model.

The fabless industry should decentralize how it offers these engineering services. Small business units (SBUs) should offer engineering services such as Circuit design engineering, Circuit layout engineering, test development engineering, failure analysis, tool manufacturing, and maintenance.

Each engineering service provider should work as an independent SBU with a maximum of 30-50 employees in each business unit. These SBUs should comply with anti-trust laws, and avoid mergers and acquisitions, which restrict competition. To avoid monopoly capitalism in the semiconductor industry, the existing shares of all major corporations should be given to employees in proportion to their productive contributions.

The next step should be to decentralize the fabless companies and make each individual business unit function independently. This means the design engineering team would become an independent business; so would the product engineering team, customer quality engineering, reliability engineering and so on. The respective businesses would operate at either lower tier or middle tier depending on their operation.

The integrated device manufacturers (IDMs) that now are privately owned also should split their fab and fabless businesses. The old fabs could function as tier 1 wafer fabs for analog chips which do not need cutting-edge transistor technology and the fabless businesses in these IDMs could be split into independent businesses to join either the middle tier or the lower tier.

Similarly, large tool manufacturing corporations should divide into SBUs and operate as independent small businesses. The wafer fab should give equal opportunities to all SBUs to compete for business, which would encourage new entrepreneurs to start their own businesses. The middle tier of the three-tier model should act as a medium to offer these services to wafer fab and also should act as the most important sector, which links the end customer (or user of electronic products and services) to upper and lower tiers of the semiconductor industry.

All engineering departments involved at the pre-silicon and post-silicon stages should have a healthy competition with one another. This would enable the end customer to get products manufactured at significantly lower costs. Such a decentralization of the fabless business would provide most innovative designs of new products.

Middle tier

The middle tier should include semiconductor businesses that work directly with end customers. This sector should include corporations with a maximum of 500 employees. This sector would interface directly with end customers, as well as with the upper business tier and the lower business tier. It would consist of co-operatively managed semiconductor companies, where the majority of company assets are owned by company employees. All corporations in this tier should have exchange relationships as a decentralized supply chain.

Chip packaging and assembly would be done in this tier, which would cooperate voluntarily with other corporations in the middle. However, those corporations that follow the model of employee sponsored corporations should be given tax incentives to attract the other players in the middle tier to follow the model of employee owned corporations. Majority shares of mid-size corporations in the middle tier would be owned by employees for them to have a stake in the success of their business.

There are many advantages of having the middle tier in the Semiconductor industry. If neo-cooperative corporations in this sector notice that customer demand is falling, then they would be able to communicate with the wafer fab at upper tier and the fabless business unit at lower tier to avoid overproduction of silicon. The upper and lower tier could use economic downturns either to cut work hours or concentrate on research and development.

With this middle tier, the neo-cooperative corporations would be able to adjust the supply and demand of electronics with a cooperative action of producers and consumers. Additionally, the middle tier would estimate consumer demand.

Another advantage of this three-tier business model would be parallel processing. The middle level could negotiate a good price for pre-silicon and post silicon services and get the work started simultaneously with shorter life cycles. This would reduce manufacturing cycle time and manufacturing costs. When economy grows, the wages of all employees also would grow. When the economy slows down, the corporations would reduce work hours across the board to avoid job cuts due to layoffs.

This three-tier business model for global Semiconductor industry would wholeheartedly accept automation in the industrial sector. Due to the use of new machines labor productivity would grow exponentially. In such a scenario the co-operative sector would be able to meet the required production target with fewer work hours but pay its workforce a higher salary in proportion to their higher productivity resulting from the use of machines.

This business model would make contributions to completely automate production of semiconductor chips from the beginning to the end which is often referred to as lights-out fab. Such a business model not only would lead the fabless semiconductor industry to the next level of innovation and financial success, but also would act as a model for other sectors in the economy leading to a vibrant growth of regional and national economies.

Apek Mulay is a senior analyst Evans Analytical Group (EAG) in Irvine, Calif. The company Website is at www.eag.com.